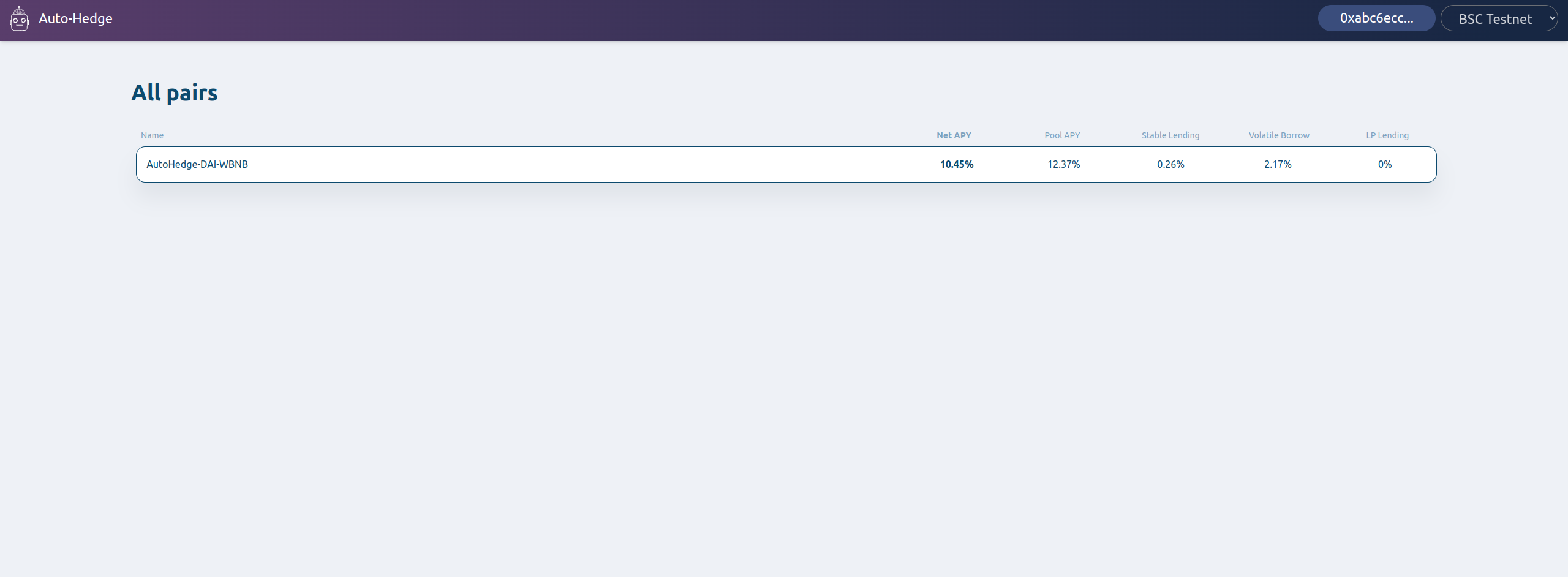

AutoHedge

AutoHedge allows you to LP on DEXes without price risk, and is immune from IL, by automatically managing a hedge against e.g. ETH in an ETH-DAI LP. The position value never goes down but gains fees. You can leverage LP - if the pair has 10% APY, you can 10x to get 100% APY

Project Description

AutoHedge

---Motive---

The general problem that exists is that people, especially VCs and more conservative institutions like hedge funds, have a bunch of cash/stablecoins lying around that they of course want to put to work to generate a return on, either temporarily while it's waiting to be invested, or more permanently, but don't want to be exposed to the price risk that's inherent in most of the DeFi yield-generating markets Since most DEX volume is not stablecoin-stablecoin pairs, that means they’re missing out on most of the market and could be getting higher returns. DNLPing (Delta-Neutral LPing) would essentially allow anyone to LP with non-stablecoin assets with an inbuilt hedge such that the position always retains the same $ value and accrues trading fees on top over time, in a 1-click tx that's as simple as regular LPing.

---How It Works - Basics---

Assuming you want to LP on say ETH-DAI with $1m of DAI and $1m of ETH:

1. Our contracts/product would take that $2m, LP at say Uniswap as usual

2. Use the LP token it receives back as collateral to borrow an amount of ETH equal to the ETH you're LPing with

3. Sell that ETH for a stable like DAI (essentially short ETH), so now you're fully hedged (and can get an additional revenue stream from lending out that DAI again). The issue at this point is that the amount of ETH that you can claim back by redeeming the LP token changes as the price of ETH changes and people add/remove ETH from the pool by trading in it.

4. We then need to regularly update the debt position to reflect the amount of ETH we have represented by the Uniswap LP token, which is where Autonomy comes in. The debt is set to automatically keep in sync with the amount of ETH in the pool. It borrows or pays back some ETH, depending on how the balance of the Uniswap pool is changing. It does this every time the debt and the ETH amounts have a difference of, say, 1%.

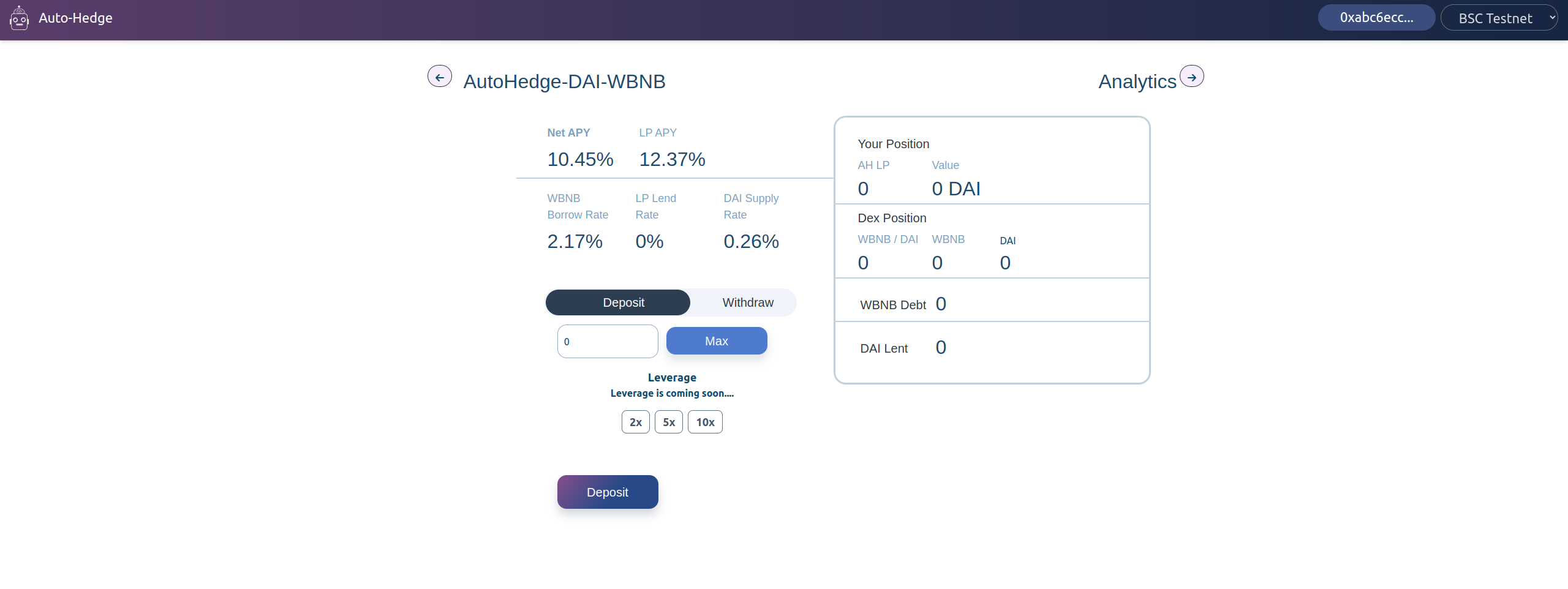

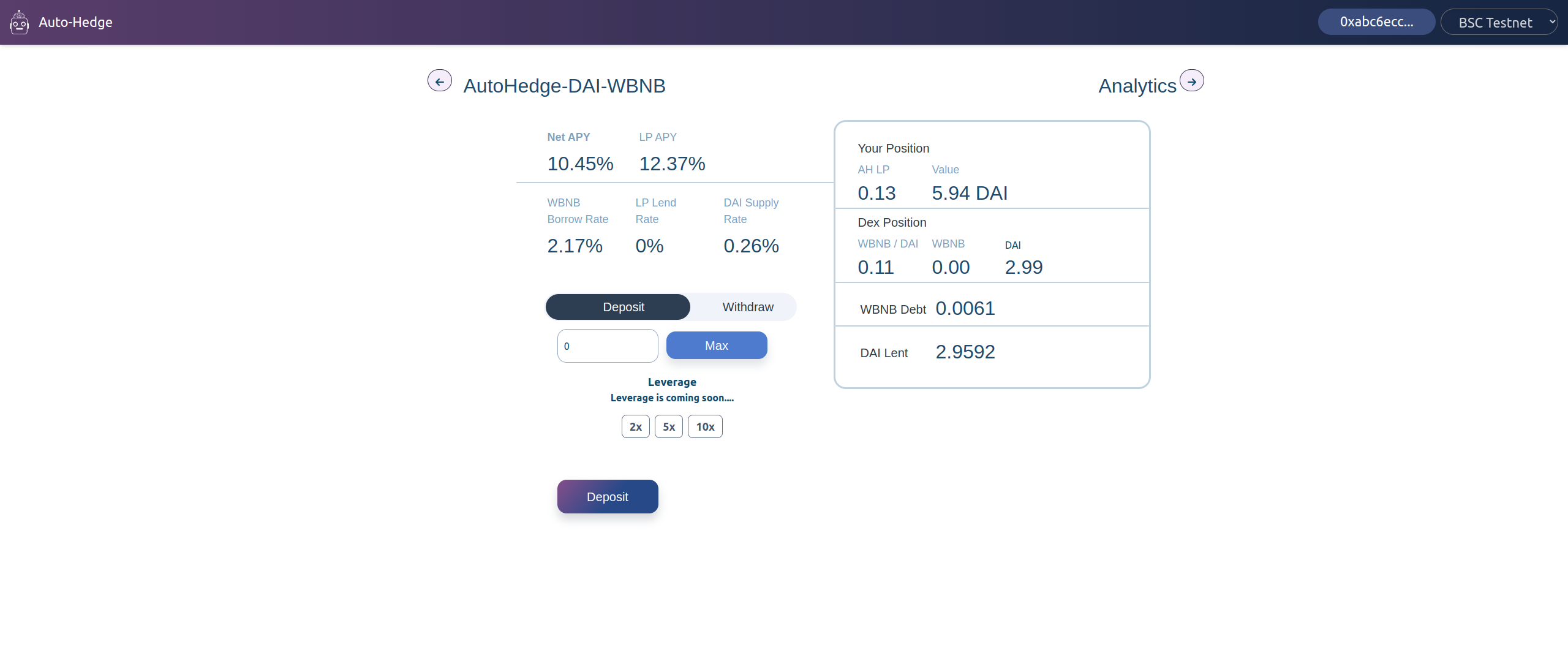

5. We can create a AH-LP (AutoHedge LP) token that wraps the Uniswap LP token, the debt, and lending positions - this is what the user directly receives and is 'the product'

This AH-LP token has some interesting properties in that it would be basically zero risk because it's always backed by 2x the value of the debt (because of the equal $ value stablecoin), and would always accrue value because it's generating trading fees but not exposed to underlying price volatility, and is therefore immune from impermanent loss (to my knowledge this is the only true solution to impermanent loss). So it's essentially delta-neutral LPing that’s immune from price volatility and IL.

If the price of ETH goes to 0, the collateral ratio is still 100%, and the user makes as much from shorting ETH as they lost from the ETH they held in the Uniswap LP.

If the price of ETH 100x’s, then:

1. the value in the LP is (100 * $1m) + $1m = $101m

2. the deb is $100 * $1m) = $100m

So it’s still fully collateralised.

---Leveraged LPing---

Because the value of the AH-LP token is, by definition, immune from price volatility, you can do something pretty insane with it. Since it can be treated like a stablecoin (with the additional perk of being yield-bearing) when used as collateral, it should therefore require a low collateral ratio to borrow against (110%?). In the example above, that means that you can take the AH-LP token that’s worth $2m and borrow ($2m / 1.1 = ) $1.81m of assets that you can then LP with again to produce more AH-LP tokens. With those $1.81m worth of AH-LP tokens, you can borrow ($1.81m / 1.1 = ) $1.65m of assets, etc. etc.

In this way, you can end up receiving the trading fees asthough you’d LP’d with $20m (10x), or more, the amount of assets, but while only having to provide $2m in liquidity. This has never been possible before because it’s never been possible to package a hedging strategy into a liquid token. It’s never been possible to package a hedging strategy into a liquid token before because there’s never been a decentralised automation protocol to remove trust and counterparty risk before.

---Liquidity - A Replacement of OlympusDAO---

Another problem that delta-neutral LPing solves is liquidity provision, especially for new/illiquid tokens. In the same way that token treasuries can monetise and utilise their tokens via OlympusDAO to increase liquidity, they can lend out large amounts of their tokens on a lending market, which enables large amounts of liquidity to be hedged, and therefore enables Autonomy’s delta-neutral strategy to be used. OlympusDAO has proven the demand for a solution to liquidity without yield farming, and delta-neutral LPing achieves the same thing without the drawbacks and risks of OlympusDAO.

Since the main barrier to people providing liquidity on a new token is price risk, this therefore removes that barrier and enables far more liquidity to be provided on DEXes for the new token.

There are 2 sources of revenue for delta-neutral LPing - trading fees and the interest from the stablecoin that was traded into from the borrowed token (the DAI in step 3. above). There is 1 cost - the interest rate paid on borrowing the volatile token. In order for delta-neutral strategies here to be possible, there needs to first be enough liquidity on lending markets to borrow enough tokens for the desired liquidity, and in order to make economic sense, we need:

LP_fees + stablecoin_interest > volatile_token_interest

LP trading fees on a new trading pair will probably be low, and therefore the interest on the volatile token needs to be low for delta-neutral LPing to make sense. Fortunately, token treasuries are in a good position to lend out large amounts of their tokens which enables enough liquidity and makes the borrowing rates very low, basically guaranteeing that delta-neutral strategies are profitable, and therefore attracting more liquidity since it can be done with very low risk for LPers. The interest that the token treasury receives will be low, but they will be providing the vast majority of the liquidity in a market to receive the vast majority of the fees, and they’re incentivised to do this for reasons other than interest rates (promoting liquidity on their token - which projects typically pay for via yield farming).

This reflects the same inputs to OlympusDAO (a token treasury locks up tokens), and achieves the same (though likely better) result of increasing a token’s liquidity on DEXes, all while the token treasury receives lending fees, but without the risks of OlympusDAO’s ponzinomics which therefore results in more liquidity.

How it's Made

Used Hardhat to test the Solidity contracts, and used React to create the UI - nothing too crazy :) It uses Uniswap as the DEX to swap and LP on, and a fork of Fuse to borrow from (Midas - they're only available on BSC testnet atm - since Fuse got hacked recently and paused all contracts)