Hybridz

Hybridz combines low and high risk option strategies for optimal Delta

Project Description

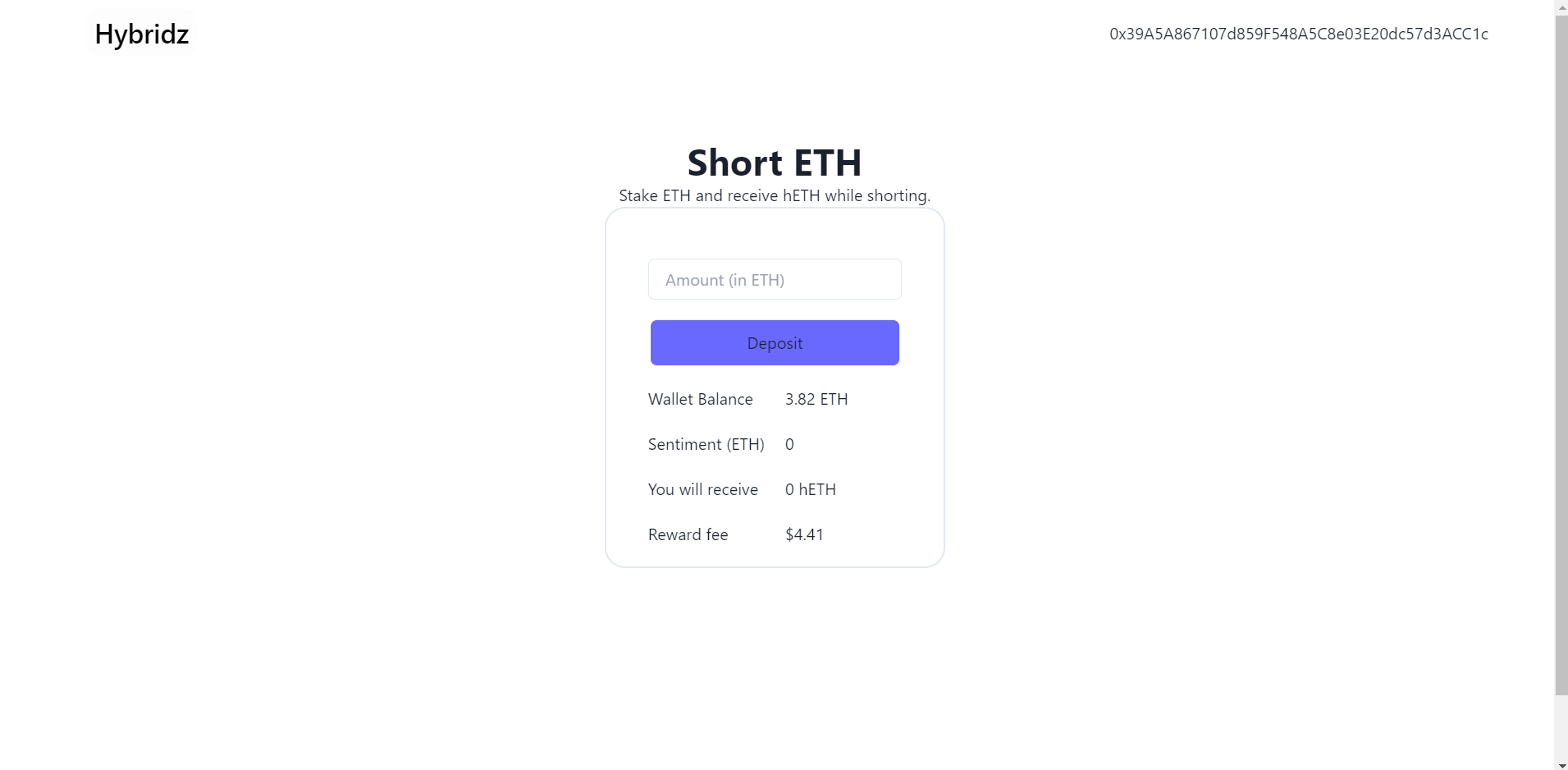

Users can view market sentiments and deposit tokens into a strategy based on their risk appetite.

Strategies gives users exposure to more complex instruments like options while combining it with less risky strategies to absorb potential losses.

Strategies are continuously tuned based on market sentiments to obtain optimal delta.

Tuning is done automatically using chainlink upkeepers.

Future goal is to have dynamic strategies that can adapt to different market conditions, always seeks to optimise the returns and to minimise potential losses.

For now we have one SHORT strategy, which is still in the making.

Here we utilise Squeeth for negative exposure to ETH, however, Squeeth only really allows delta neutral strategies. So we combine this with Aave to tweak the delta to our liking.

Lastly we deposit the aTokens in a curve pool and the crvLP in Yearn for extra yield on our idle assets.

The ratios are controlled by a targetDelta, targetCollateralRatio and targetHealthFactor. These are of course intertwined and will (in future) be condensed even more using some fancy math.

Idea is that strategy would be dynamic enough to adjust its positions, collateral and debt, only by changing the targetDelta variable.

Goal: We want short exposure to Ethereum, with possiibility of delta neutral if market conditions changes.

How: using Opyns Squeeth vaults to mint power perpetual tokens, we can get a slightly negative exposure to ETH. However, we have to use ETH as collateral to mint these tokens and setting Delta too low will cause us to get liquidated if volatile markets. So we swap the powerPerpetual tokens for DAI (delta neutral=earning funding rate) we then use Aave to deposit our DAI as collateral, we borrow ETH, swap the ETH for DAI and deposit the DAI as collateral, while maintaining our target health factor. We then receive aDAI from Aave, we deposit this in curves aToken pool for extra yield, we then receive curveLPs that we can deposit into yearn who then deposits it into convex for extra yield.

To untangle this when changing target ratios is of course costly but not too complicated. We are still working on how to do it as smooth as possible, doing it with a flashloan might be the most secure way.

Current strategy will:

1. open a Squeeth vault

2. supply ETH as collateral at Squeeth vault

3. mint oSQTH tokens

4. sell oSQTH for DAI (= negative exposure on ETH)

5. supply DAI at Aave

6. take ETH loan at Aave

7. swap ETH for DAI

8. supply DAI at Aave

9. supply aDAI at Yearn/Curve

9. keep track of collateral ratio (CR) at Squeeth

10. keep track of health factor (HR) at Aave

11. check for delta adjustments made by strategy manager

11. automated with chainlink upkeepers

Future for Hybridz

integrate aave V3 multichain supplying/borrowing for best rates.

create strategies that are dynamic enough to adjust to any market condition by changing the target delta.

introduce more market sentiment and prediction tools to better tune strategies.

How it's Made

Strategy utilises followiing onchaini protocols:

1. OpynV2 SQUEETH vaults for short position on ETH

2. AAVE V3 for leverage short positon on ETH

3. CHAINLINK upkeepers for collateral- and DELTA adjustments

4. YEARN/CURVE for stable returns on aDAI

not yet implemented:

5. EPNS for notification on collateral/DELTA/market adjustments

6. apWine for aToken

The sentiment/ prediction analysis:

We are using BISON's Sentiment.

"The machine learning algorithm evaluates over two million tweets from the crypto community. It then filters out those that do not add any value to the analysis because they are spam or something similar. About 250,000 tweets remain and are visually processed by the BISON algorithm in the Sentiment"

On top of it we have capabilities to customize the sentiments based on the user preference feeds.