dVIX

A protocol for making decentralized volatility index feeds for synthetic tokens.

Project Description

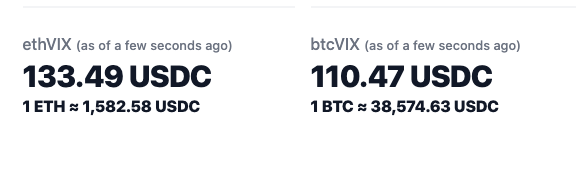

dVIX or decentralized volatility index is a protocol for the building of model-free, near real-time volatility index feeds of any decentralized or centralized asset that has a robust derivatives market. dVIX uses a modified CBOE VIX formula for calculating volatility, the current gold standard. This proof-of-concept version is designed to make volatility synthetics on UMA. Therefore, dVIX also provides two simple tools for the UMA Data Verification Mechanism; an API call and spreadsheet.

How it's Made

For the proof-of-concept real time options data is pulled from Deribit. Exchange rate and interest rate data is pulled from AAVE. This is put through the adapted CBOE VIX algorithm which generates the ETHVIX and BTCVIX feeds.

The following are two pieces that we did not finish but that we want to highlight as partial work:

-

Using IPFS and OrbitDB for the data.

-

Launching synthetic ETHVIX and BTCVIX tokens on UMA.