Universe Finance Backtesting for Uniswap V3

Universe Finance Backtesting system is the first open source backtesting platform for Uniswap V3. Our comprehensive database allows all developers to test their strategy in a work smarter way!

Project Description

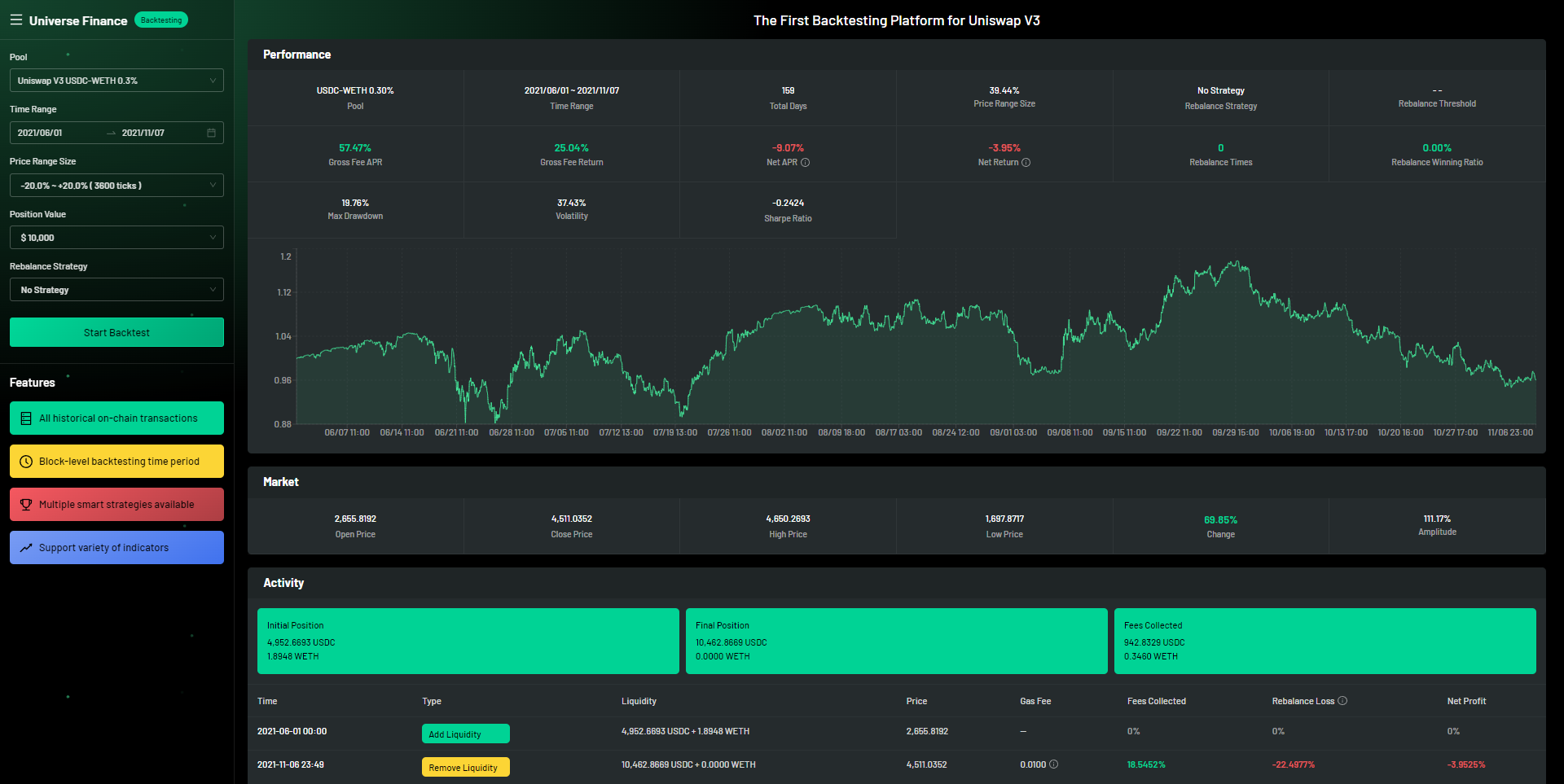

- According to K-line data, we can simulate the price information of a specified block, all based on Uniswap's real transactions;

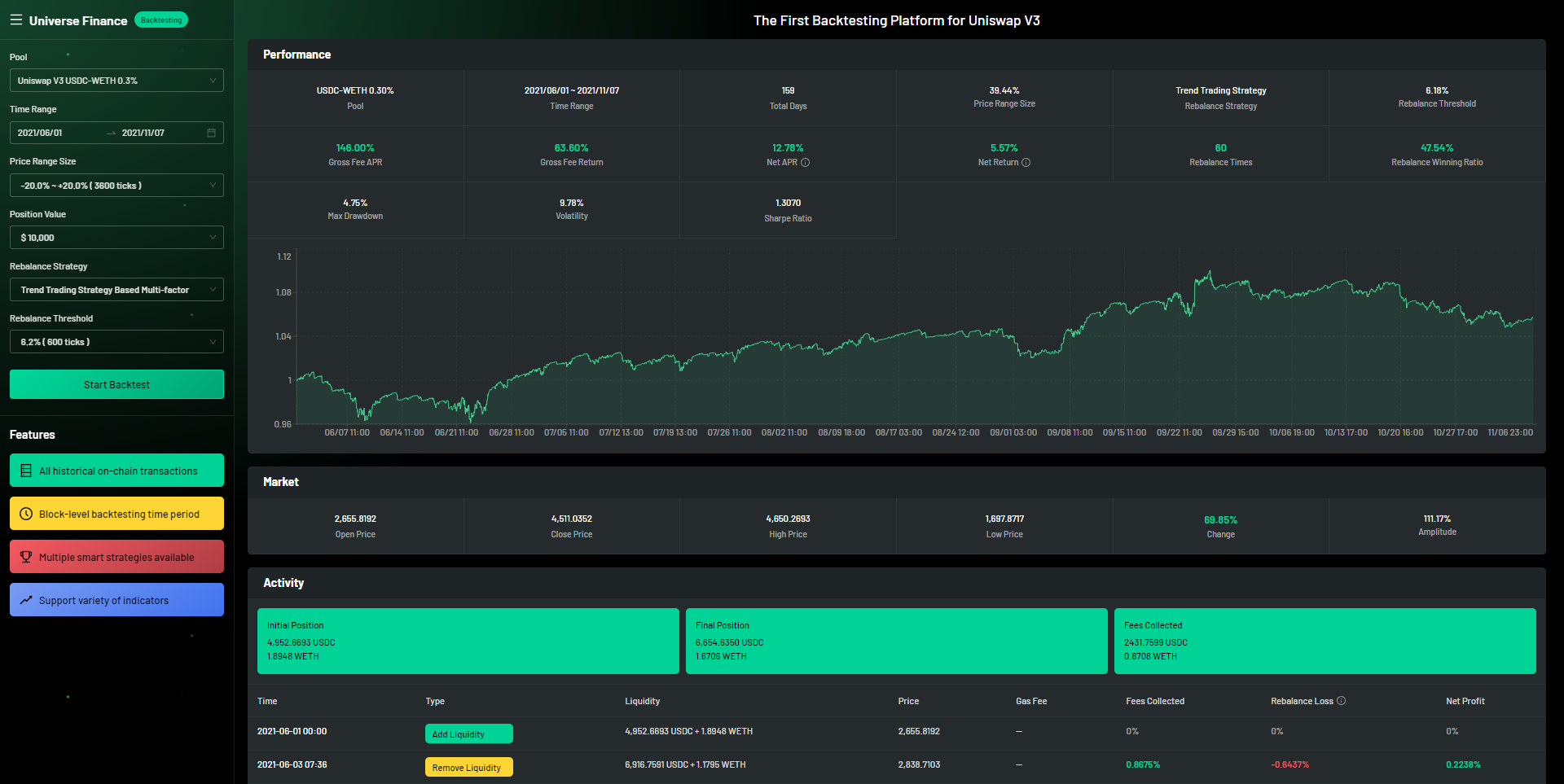

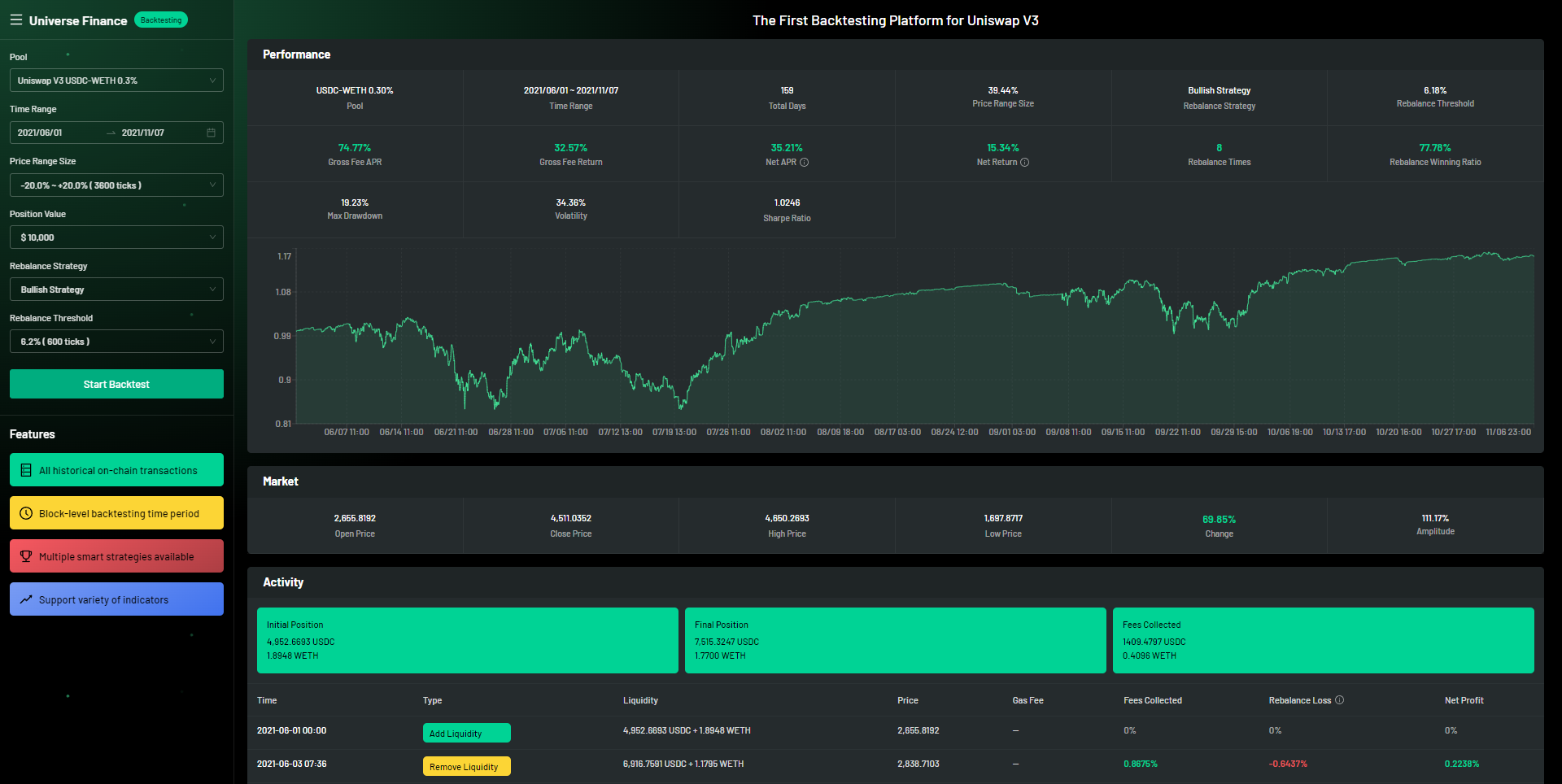

- Based on the swap and other records of Uniswap V3 pools, the signals can be produced by prefixed strategies or customized strategies by users, and we can simulate the procedure of adding/removing liquidity ;

- By recording all these data and the initial principles from users, the backtesting system will generate the performance details in graphs as well as in transactions logs for the strategy.

How it's Made

After the release of Uniswap V3, we built a financial model which simulate the impermanence loss based on price range and price deviation. In that back-testing system, we calculate the gross fee APR of USDC-ETH pair. From those data, we come to the conclusion that LPs have a chance to earn more money by using version3 than version2. In order to get more intuitive and specific quantitative data, we delivered the back-testing system to verify our views.

Except for the Uni-V3 Liquidity provider back-testing system, we also implied our own Trend Trading Strategy Based Multi-factor Rebalance strategy into real product which is our current site of https://www.universe.finance/vaults

The whole backtesting system is based on Uniswap V3. All the data is from Uniswap V3 and it won't be possible until Uniswap released the liquidity management feature.

We made our backtesting system open source and we also studied from Visor's doc and on-chain strategy data in order to improve the backtesting system.

This project is based on Java version 1.8 and Gradle version 7.1.

I am impressed that the team made the backtesting system and made it open source for the whole industry.